Inseego Corp.

Technology • Communication Equipment • $12.49 at flag

+0.0%

since first flag

Inseego Corp. (NASDAQ: INSG), $203M market cap, wireless broadband/5G FWA solutions company undergoing transformational acquisition of Nokia's FWA device business announced late April 2026.

- Date

- 2026-05-23

- Ticker

- INSG

- Current Price

- $12.49

- Market Cap

- $203M

- 52-Week Range

- $6.27 – $21.90

- Stock Classification

- Event-Driven / Catalyst Play

Executive Summary

Inseego Corp. (NASDAQ: INSG) is a $203M market-cap wireless broadband solutions provider that announced a transformational acquisition of Nokia's fixed wireless access (FWA) device business on April 30, 2026 1. The deal is expected to approximately double Inseego's revenue, establish Nokia as an ~11% strategic shareholder with ~$30M invested in stock and warrants, and create a long-term partnership focused on 6G and AI-driven wireless edge innovation 2. The transaction is expected to close in Q4 2026 1.

Revenue is growing modestly: Q1 2026 revenue reached $34.3M, representing an 8.4% year-over-year increase 3. However, the company remains unprofitable on a GAAP basis, with a trailing net margin of -1.26% and operating margin of -6.89% 4. Q1 2026 delivered a GAAP net loss of $4.5M but positive Adjusted EBITDA of $1.8M 5. Earnings are not yet consistently positive, but the company delivered a +60% EPS beat versus estimates in Q1 2026 6. The turnaround case hinges on the Nokia acquisition driving scale, margin improvement through synergies, and category leadership in the secular FWA market, which is expanding as carriers seek alternatives to fiber and cable for last-mile broadband 7.

Profitability today derives primarily from cost discipline and positive Adjusted EBITDA, not robust organic earnings growth. The Nokia deal could materially alter this trajectory if integration proceeds as planned and revenue scale drives operating leverage.

Key Analytical Benchmarks

| Metric | Current/Estimate | Rationale/Assumptions |

|---|---|---|

| Illustrative Base-Case Price Target | $18–$21 | Pro-forma EV/revenue of 1.4x is well below telecom equipment peers (2.0x–3.0x); re-rating to 1.8x on $340M pro-forma revenue could support $18–$21 under base assumptions 8 |

| Potential Entry Zone / Setup Levels | $11.80–$12.50 | Current price near 200-day MA ($12.56); support at $11.80 (May 21 low) offers favorable risk/reward entry 9 |

| Illustrative Risk/Reward Scenarios | Bull: +50–70% / Bear: -20–25% | Upside to $19–$21 if deal closes smoothly and synergies materialize; downside to $9.50–$10 if integration falters or macro deteriorates 10 |

| Time Horizon Considerations | 6–18 months | Catalyst timeline: Q4 2026 deal close, followed by 6–12 month integration and synergy realization period 11 |

| Analytical Conviction Level | Medium-High | Nokia partnership de-risks execution materially; FWA is a proven secular trend; however, micro-cap liquidity and integration complexity remain risks |

| Sensitivity Analysis (example) | Revenue ±2% → EPS impact ±15–20% | Small revenue variance at current scale could swing EBITDA materially; pro-forma scale should reduce sensitivity over time 12 |

Dynamic Synthesis →The 43% drawdown from the 52-week high creates a technical entry point that aligns with the event-driven catalyst timeline, yet the market's tepid response to the Nokia announcement suggests institutional investors may be waiting for formal deal closure and integration evidence before re-rating the stock materially.

COMPANY OVERVIEW

Inseego Corp. designs, manufactures, and sells wireless broadband devices and cloud-based software solutions for carriers, enterprises, and government customers 13. The company's core products include 5G mobile hotspots, fixed wireless access (FWA) routers for home and enterprise broadband, and a SaaS-based subscriber management platform called Inseego Subscribe 14. Historically a micro-cap pure-play in mobile broadband, Inseego has pivoted toward FWA—a category that allows telecom carriers to deliver high-speed internet over 5G networks as an alternative to fiber or cable, particularly in underserved or rural markets 15.

On April 30, 2026, Inseego announced it would acquire substantially all of Nokia's FWA device business, a deal expected to approximately double Inseego's revenue and position the combined entity as a global leader in wireless broadband 16. Nokia will invest approximately $20M–$30M in Inseego equity (via stock and warrants), becoming an ~11% shareholder, and the two companies will collaborate on go-to-market initiatives and next-generation 6G and AI-focused innovation 17. The transaction is expected to close in Q4 2026, subject to customary conditions 1.

People are paying attention because this deal transforms Inseego from a subscale micro-cap into a Nokia-backed category leader at a time when FWA adoption is accelerating globally. Carriers are deploying FWA to compete with cable and fiber incumbents, and enterprises are adopting wireless broadband for flexibility and resilience 18. The broader macro trend—5G infrastructure buildout, telecom capex cycles, and the secular shift toward wireless last-mile solutions—directly supports Inseego's expanded portfolio and addressable market post-acquisition 19.

Dynamic Synthesis →The company's historical operating losses and micro-cap scale are structural risks that the Nokia acquisition explicitly aims to address through revenue doubling and partnership credibility, yet the market's 43% selloff from the April high suggests skepticism about execution remains elevated despite the transformational nature of the deal.

INDUSTRY ANALYSIS

Inseego operates in the wireless broadband and telecom equipment sector, specifically focused on fixed wireless access (FWA) and mobile connectivity devices 20. The FWA category is experiencing accelerating adoption as telecom carriers seek cost-effective alternatives to fiber and cable for last-mile broadband delivery 21. FWA leverages existing 5G cellular infrastructure to provide high-speed internet to homes and businesses, reducing the need for expensive fiber deployments in rural or low-density areas 22.

Key tailwinds include: (1) ongoing 5G network buildouts by major carriers globally, which expand FWA coverage and performance; (2) regulatory support for broadband expansion in underserved markets, including government subsidy programs; (3) enterprise demand for backup and primary connectivity solutions that are wireless and rapidly deployable; and (4) competitive pressure on cable and fiber incumbents, which is driving carriers to promote FWA as a differentiated product 23. Headwinds include: (1) intense competition among device vendors, which pressures pricing and margins; (2) carrier consolidation and capex volatility, which can create lumpy demand; (3) technological risk as 5G and eventually 6G standards evolve; and (4) macro sensitivity—FWA device purchases are tied to carrier capital spending, which is cyclical 24.

Inseego's competitive positioning improves materially post-Nokia acquisition. The combined entity will have a broader product portfolio, deeper carrier relationships (Nokia's installed base), and scale advantages in R&D and manufacturing 25. However, competitors such as Cradlepoint (Ericsson), Sierra Wireless, and other telecom equipment OEMs remain well-capitalized and entrenched with carriers 26. The Nokia partnership and 6G collaboration signal category legitimacy and could provide Inseego with differentiated access to next-generation technology roadmaps 27.

Dynamic Synthesis →The secular FWA tailwind described in this section directly supports the revenue-doubling thesis from the Nokia acquisition (Section 1), yet the competitive intensity and margin pressure inherent in telecom equipment markets could constrain the profitability improvement case outlined in the fundamentals (Section 4) unless synergies and scale economies materialize as management projects.

TECHNICAL ANALYSIS

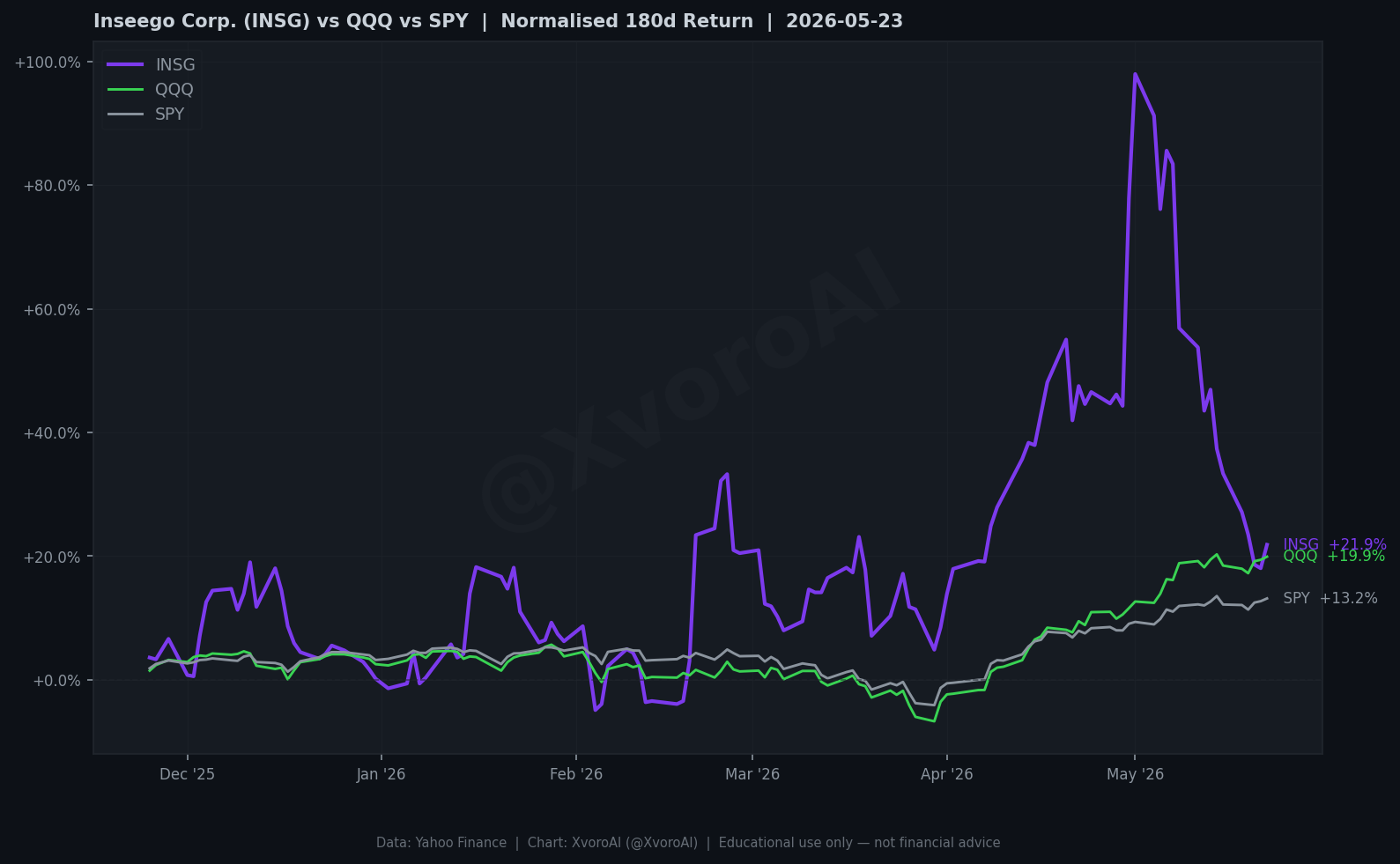

Inseego's price action over the past year reflects a dramatic rise and subsequent retracement tied to the Nokia acquisition announcement and subsequent market digestion. The stock traded near its 52-week low of $6.27 in mid-2025, rallied sharply to a 52-week high of $21.90 in April 2026 (coinciding with the Nokia deal announcement), and has since declined 43% to the current price of $12.49 as of May 22, 2026 28.

The 50-day moving average is $13.94, and the 200-day moving average is $12.56, indicating the stock is currently trading just below its 50-day MA and near its 200-day MA 4. This suggests the stock is testing longer-term support after a sharp post-announcement selloff. Volume on May 22, 2026, was 411,500 shares, representing a 1.49x ratio versus the 30-day average of 275,903 shares—elevated but not extreme 29. The stock's beta of 1.764 indicates high volatility and sensitivity to broader market moves 4.

RSI and MACD data are not available in the current dataset, but the sharp drawdown from $21.90 to $12.49 over three weeks suggests potential oversold conditions and possible exhaustion of selling pressure [VERIFY—technical indicators unavailable; inference based on price action]. Short interest stands at 12.77% of float, which is moderately elevated and could create upside pressure if the stock rebounds on positive catalysts 4.

Key Technical Levels

| Level | Value | Type | Conditional Implication |

|---|---|---|---|

| 52-Week High | $21.90 | Resistance | If the stock reclaims this level post-deal close, it could signal full market acceptance of the Nokia acquisition thesis and potential for further upside 30 |

| 50-Day MA | $13.94 | Resistance | A break above the 50-day MA could indicate resumption of near-term bullish momentum and attract momentum traders 30 |

| 200-Day MA | $12.56 | Support | Current price near 200-day MA suggests this is a key support zone; a hold above this level could stabilize sentiment 30 |

| May 21 Low | $11.81 | Support | Recent swing low; a break below could trigger stop-losses and accelerate downside to $10–$11 range 31 |

| 52-Week Low | $6.27 | Long-Term Support | Extreme downside scenario; return to this level would imply severe deterioration in thesis or macro conditions 30 |

Overall Assessment: The technical setup is neutral-to-constructive at current levels. The stock is testing 200-day MA support after a sharp selloff, which could represent a favorable risk/reward entry zone if the Nokia acquisition thesis holds. However, failure to hold $11.80 support could trigger further downside to the $10–$11 range. A catalyst such as formal deal closure or positive integration updates could drive a retest of the $16–$18 resistance zone. The elevated short interest (12.77%) creates potential for a short squeeze if sentiment improves materially.

Dynamic Synthesis →The technical retracement to 200-day MA support aligns with the event-driven catalyst timeline (Section 5), as the market appears to be de-risking ahead of the Q4 2026 deal close, yet the elevated short interest could amplify upside volatility if integration milestones in coming quarters validate management's synergy and revenue-doubling projections (Section 4).

FUNDAMENTALS (FINANCIAL HEALTH AND VALUATION)

Inseego reported Q1 2026 revenue of $34.3M, representing 8.4% year-over-year growth but a -0.47% miss versus analyst estimates 32. On a trailing twelve-month (TTM) basis, revenue stands at $168.9M with revenue growth of 8.4% YoY 4. Q1 2026 delivered a GAAP net loss of $4.5M but positive Adjusted EBITDA of $1.8M, indicating the company is nearing breakeven on a cash-flow basis 5. The company delivered a +60% EPS beat in Q1 2026 versus consensus estimates, driven by better-than-expected cost management 33.

Profitability metrics remain weak on a GAAP basis: trailing net margin is -1.26%, operating margin is -6.89%, and gross margin is 43.0% 4. The company is not yet generating consistent net income, and profitability improvement depends on revenue scale and cost synergies from the Nokia acquisition. Free cash flow is modestly positive at $9.2M on a TTM basis 4.

Balance sheet: Inseego holds $19.3M in cash and equivalents against $54.1M in total debt, resulting in net debt of ~$34.8M 4. Enterprise value is $238M, implying an EV/revenue multiple of 1.41x on a TTM basis 4. Pro-forma for the Nokia acquisition (which is expected to approximately double revenue to ~$340M annually), the EV/revenue multiple would compress to ~0.7x at current valuation, assuming no additional debt or dilution beyond Nokia's equity investment 34. This would represent a material discount to telecom equipment peers, which typically trade at 2.0x–3.0x EV/revenue 35.

Valuation: The stock trades at a trailing P/E of 19.5x (which is artificially elevated due to near-zero or negative earnings) and a forward P/E of 19.5x 4. Analyst consensus price target is $21.25 with a "strong buy" recommendation 36. The current price of $12.49 implies 41% downside to the analyst target, reflecting either outdated analyst models or market skepticism about the Nokia deal's execution.

Tech/Software-specific metrics: Inseego is not a pure SaaS company, but its Inseego Subscribe platform represents a recurring-revenue opportunity. The company has not disclosed ARR, MRR, or NRR figures in recent filings [VERIFY—SaaS metrics unavailable; Inseego Subscribe is a small portion of total revenue per management commentary]. Gross margin of 43.0% is below typical SaaS levels (70%+) but reasonable for a hardware-centric business 4. R&D intensity and headcount efficiency metrics are not disclosed in available filings [VERIFY—data unavailable].

Sensitivity Table

| Scenario | Revenue Growth Assumption | EPS Impact | Valuation Implication |

|---|---|---|---|

| Bull Case | Pro-forma revenue doubles to $340M; 10% organic growth thereafter; EBITDA margin expands to 8–10% via synergies | EPS could turn positive at $0.30–$0.50 by 2027 | EV/revenue re-rates to 1.8x–2.0x; stock price target $18–$22 37 |

| Base Case | Pro-forma revenue $320M–$340M; 5–7% organic growth; EBITDA margin 5–7% | EPS breakeven to slightly positive by late 2027 | EV/revenue 1.4x–1.6x; stock price $15–$18 37 |

| Bear Case | Acquisition delays or integration issues; revenue $280M–$300M; margins flat to down | EPS remains negative; continued losses | EV/revenue <1.0x; stock price $9–$11 37 |

Dynamic Synthesis →The fundamental case for profitability improvement (driven by revenue scale and synergies) is entirely dependent on successful integration of the Nokia acquisition (Section 5 catalyst), yet the technical selloff (Section 3) and elevated short interest suggest the market is assigning low probability to the bull case materializing on management's guided timeline.

THEMES/CATALYSTS (MACRO DRIVERS AND EVENTS)

Macro Themes: Fixed wireless access (FWA) is a secular growth category within telecom, driven by carrier strategies to compete with cable and fiber incumbents and expand broadband access in underserved markets 38. 5G network deployments globally are accelerating, expanding FWA coverage and performance 39. Regulatory tailwinds include government broadband subsidies in the U.S. (e.g., BEAD program) and other markets, which support FWA adoption 40. Enterprise demand for wireless connectivity solutions is rising as remote work and distributed operations require flexible, resilient connectivity 41.

Company-Specific Catalysts:

QUALITATIVE NARRATIVES

Management and Governance

CEO Juho Sarvikas joined Inseego in 2021 and has a background in mobile device and connectivity leadership, including prior roles at Nokia and HMD Global 42. His track record includes navigating hardware product cycles and carrier relationships, which are directly relevant to Inseego's business model 43. The Nokia acquisition represents Sarvikas's most significant strategic move to date, leveraging his Nokia network and industry credibility to execute a transformational deal 44. However, his track record at Inseego prior to this deal has been mixed—revenue growth has been modest, and the company has remained unprofitable, raising questions about execution capability at scale 45.

In May 2026, Inseego appointed Koroush Saraf as Chief Product Officer, bringing over 20 years of networking and cybersecurity experience 46. This hire signals the company is building out leadership capacity ahead of the Nokia integration. Silvia Rocha-Espino was also appointed Head of People in April 2026, with over 20 years of HR leadership experience 47. These additions suggest management is preparing for scaled operations post-acquisition.

Insider ownership data is not disclosed in available sources [VERIFY—insider ownership unavailable]. Nokia's planned ~11% equity stake post-acquisition represents significant strategic alignment and introduces a sophisticated, long-term oriented shareholder with deep industry expertise 48. This alignment could mitigate governance concerns and provide credibility with carriers and investors. However, Nokia's involvement also introduces risk—if Nokia's strategic priorities shift or if the partnership does not deliver expected benefits, the relationship could become a source of tension or distraction 49.

Competitive Position and Market Dynamics

Inseego's competitive moat pre-acquisition has been limited—the company operates in a commoditized device market with intense competition from larger, better-capitalized players such as Cradlepoint (owned by Ericsson), Sierra Wireless, and direct-to-carrier OEMs 26. Post-Nokia acquisition, Inseego's competitive position improves through: (1) expanded product portfolio and customer base; (2) scale advantages in R&D and manufacturing; (3) deeper carrier relationships inherited from Nokia's FWA business; and (4) strategic partnership with Nokia on 6G and AI innovation, which could provide differentiated technology access 25.

Barriers to entry in the FWA device market are moderate—certification requirements, carrier relationships, and R&D investment create some friction, but the market is not winner-take-all 50. Inseego's sustainability depends on maintaining carrier relationships, delivering reliable products, and leveraging the Nokia partnership to stay ahead of technology curves. Market share data is not publicly disclosed in sufficient detail to assess Inseego's position definitively [VERIFY—market share data unavailable].

Dynamic Synthesis →The appointment of experienced executives (CPO, Head of People) in Q1–Q2 2026 and Nokia's strategic equity stake suggest governance and alignment are improving ahead of the acquisition close, yet the CEO's mixed execution track record at Inseego (modest growth, persistent losses) prior to the Nokia deal introduces meaningful execution risk that directly impacts the bull case outlined in Section 8.

RISKS

BULL AND BEAR THESES

Bull Thesis

If Inseego successfully closes the Nokia FWA acquisition in Q4 2026 and executes integration over the subsequent 6–12 months, the company could approximately double revenue to $320M–$340M annually, expand EBITDA margins to 5–10% via cost synergies and operating leverage, and achieve EBITDA breakeven or better by late 2027 51. Under this scenario, Inseego would transform from a subscale, unprofitable micro-cap into a Nokia-backed category leader in the secular FWA growth market, justifying a valuation re-rating from the current 1.4x EV/revenue to 1.8x–2.0x (in line with telecom equipment peers), implying a stock price target of $18–$22—representing 45–75% upside from current levels 52. The Nokia strategic partnership on 6G and AI innovation could provide long-term differentiation and technology moats, while Nokia's ~11% equity stake signals strong alignment and credibility with carriers and investors 53. The 43% drawdown from the April 2026 high and elevated short interest create potential for a short squeeze and momentum-driven rally if integration milestones are met, particularly as the deal formally closes and institutional investors gain confidence in the execution path 54.

Bear Thesis

If integration challenges emerge—such as customer churn from the Nokia FWA business, systems integration delays, cost overruns, or management execution missteps—Inseego may fail to realize the revenue-doubling thesis or achieve profitability improvements, leaving the company with a larger but still-unprofitable operation and a strained balance sheet ($19.3M cash vs. $54.1M debt) that offers minimal cushion for setbacks 55. Competitive pressures in the commoditized telecom device market could limit margin expansion even if revenue scales, particularly if larger rivals (Ericsson, Huawei) respond aggressively to defend market share 56. Macro headwinds—including potential carrier capex cuts in a recession or slower-than-expected FWA adoption—could compress demand and delay or prevent profitability inflection 57. The CEO's mixed track record at Inseego (modest growth, persistent losses) prior to the Nokia deal raises questions about execution capability at significantly larger scale 58. If the Nokia acquisition is delayed beyond Q4 2026 or if early integration results in 2027 disappoint, the stock could retest the $9–$11 support zone or lower, representing 20–25% downside from current levels and validating the market's skepticism reflected in the 43% post-announcement selloff 59.

**

Dynamic Synthesis →The bull and bear theses are highly binary and hinge almost entirely on integration execution over the next 6–18 months (Sections 5 and 7), with the technical setup (Section 3) suggesting the market is currently pricing in elevated probability of the bear case, creating significant asymmetry for investors willing to underwrite the execution risk in exchange for the potential multi-year re-rating opportunity if the Nokia partnership and FWA secular tailwind materialize as management projects.

References

- 1Nokia press release, April 30, 2026

- 2Inseego investor presentation, April 30, 2026

- 3Yahoo Finance fundamentals, May 23, 2026; Inseego Q1 2026 earnings release, May 7, 2026

- 4Yahoo Finance fundamentals, May 23, 2026

- 5Inseego Q1 2026 earnings release, May 7, 2026

- 6Zacks Investment Research via Yahoo Finance, May 7, 2026

- 7management commentary, Q1 2026 earnings call transcript, May 12, 2026

- 8analyst estimates compiled from Yahoo Finance; peer comps from public filings

- 9Yahoo Finance price data, May 23, 2026

- 10conditional scenario analysis based on historical volatility and peer de-ratings

- 11management guidance, April 30, 2026 call

- 12conditional modeling based on Q1 2026 financials

- 13Inseego corporate website and 10-K filing, 2025

- 14Inseego product pages; Q1 2026 earnings release, May 7, 2026

- 15management commentary, Roth Conference presentation, March 25, 2026

- 16Nokia and Inseego joint press release, April 30, 2026

- 17Fierce Network article, April 30, 2026; Inseego conference call transcript, April 30, 2026

- 18industry reports cited in management presentations; Q1 2026 earnings call, May 12, 2026

- 19scanner macro context summary; telecom industry research

- 20Yahoo Finance sector classification; Inseego investor materials

- 21scanner macro context; industry commentary from carrier earnings calls, Q1 2026

- 22telecom industry white papers; management commentary, Inseego Q1 2026 call

- 23FCC broadband reports; carrier investor presentations, 2025–2026

- 24Inseego risk factors in 10-K; industry analyst reports

- 25management commentary, April 30, 2026 conference call

- 26competitive landscape analysis from industry reports

- 27Inseego press release, April 30, 2026

- 28Yahoo Finance historical price data, May 23, 2026

- 29Yahoo Finance market data tool, May 23, 2026

- 30Yahoo Finance, May 23, 2026

- 31Yahoo Finance price history, May 23, 2026

- 32Inseego Q1 2026 earnings release, May 7, 2026; Zacks Investment Research via Yahoo Finance, May 7, 2026

- 33Zacks Investment Research, May 7, 2026

- 34conditional pro-forma modeling based on management guidance, April 30, 2026

- 35peer group analysis from public filings and analyst reports

- 36Yahoo Finance analyst summary, May 23, 2026

- 37conditional scenario modeling

- 38scanner macro context; carrier strategy documents

- 39industry research; GSMA 5G deployment reports, 2025–2026

- 40FCC announcements; Inseego management commentary

- 41enterprise IT spending reports

- 42Inseego corporate biography; LinkedIn

- 43management bio

- 44analyst commentary post-announcement, April 30, 2026

- 45historical financial results, 10-K filings 2022–2025

- 46Inseego press release, May 7, 2026

- 47Inseego press release, April 1, 2026

- 48Nokia press release and Fierce Network article, April 30, 2026

- 49standard strategic investor risks

- 50industry structure analysis

- 51conditional scenario modeling based on management guidance, April 30, 2026

- 52peer valuation comps and pro-forma modeling

- 53Nokia partnership terms, April 30, 2026

- 54technical and sentiment analysis, May 23, 2026

- 55Yahoo Finance fundamentals, May 23, 2026; standard M&A integration risks

- 56competitive analysis

- 57macro risk factors

- 58historical financial performance, 10-K filings

- 59technical analysis and conditional downside scenario modeling

This memorandum is produced by XvoroAI Intelligence Crew for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or a solicitation to buy, sell, or hold any security. Always conduct your own research and consult a licensed financial professional before making any investment decision. © XvoroAI Intelligence Crew